Tax season used to be a handoff, but now we find consumers are no longer defaulting to CPAs or waiting for professional guidance. They are learning, validating, and executing tax strategies themselves, often in the same place they get product reviews and financial advice. The shift is not subtle, and it is not temporary.

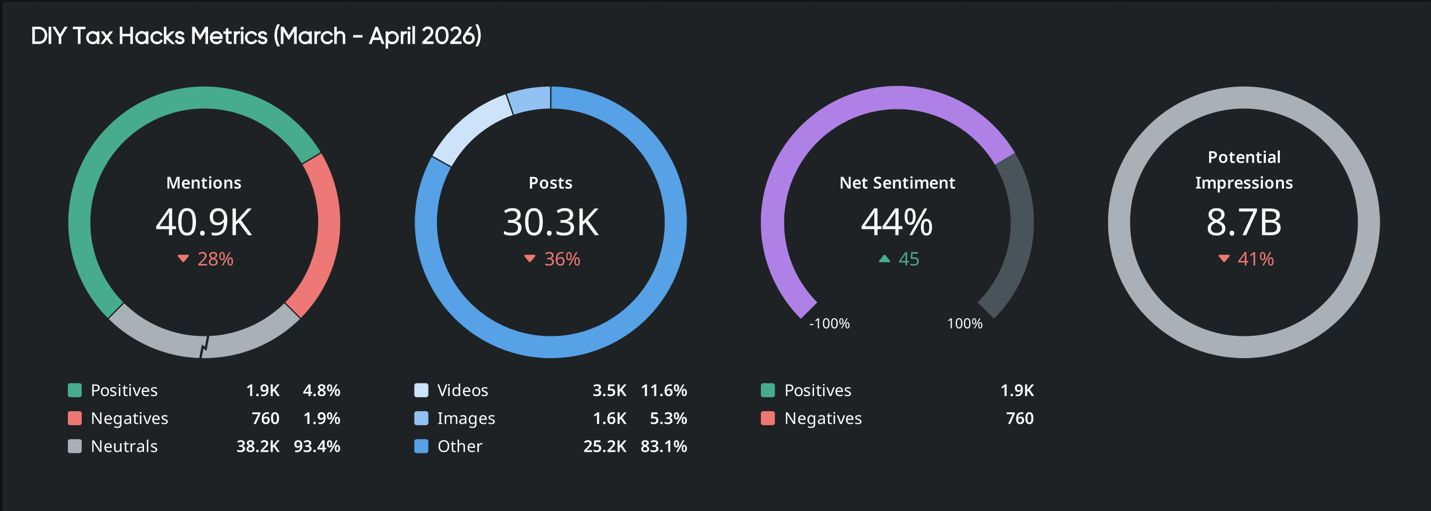

From the Quid dashboard, the scale makes that clear. There are 40.9K mentions and 30.3K posts tied to DIY tax behavior within a single window, paired with 8.7 billion potential impressions. Sentiment sits at 93.4% neutral, which signals something more important than excitement. It signals normalization.

This isn’t just a spike, it’s a baseline. And it is being reinforced by structural changes, not just social ones.

From the Quid Agent’s TikTok analysis, we know that new deductions tied to Schedule 1 A are actively incentivizing consumers to file independently. Overtime, tips, and vehicle-related claims are creating immediate financial motivation, and the content ecosystem is translating those rules into fast, repeatable actions.

What looks like “DIY tax hacks” is actually something more durable. It is a shift in who owns financial decision-making.

The shift is not coming from creators alone. It is being triggered upstream.

From the Quid Agent we’ve uncovered:

This dynamic creates a feedback loop that reinforces itself.

Policy introduces new layers of complexity, often faster than most people can reasonably interpret. Platforms respond by simplifying those changes into guided workflows and pre-filled experiences. Creators step in next, translating those simplified pathways into fast, highly shareable explanations, some accurate, some not.

Consumers then act on that information immediately, often without verifying the details, because the path appears clear and the incentive feels urgent. The cycle repeats, gaining speed with each iteration.

And in that environment, speed consistently outpaces accuracy.

The shift toward DIY tax behavior is not happening because people suddenly became experts. It is happening because the tools are doing more of the work.

According to the Quid Agent analysis, automation has eliminated much of the friction that once justified professional support. Pre-fill systems, mobile-first filing, and guided workflows now handle the foundational steps that once required manual input and interpretation.

Platforms are also quietly expanding into “do it for me” tiers, blurring the line between assisted filing and full-service support while still presenting the experience as DIY. Features like photo uploads for W-2s and 1099s, automated accuracy checks, and step-by-step flows are conveniences that are standardizing how people file.

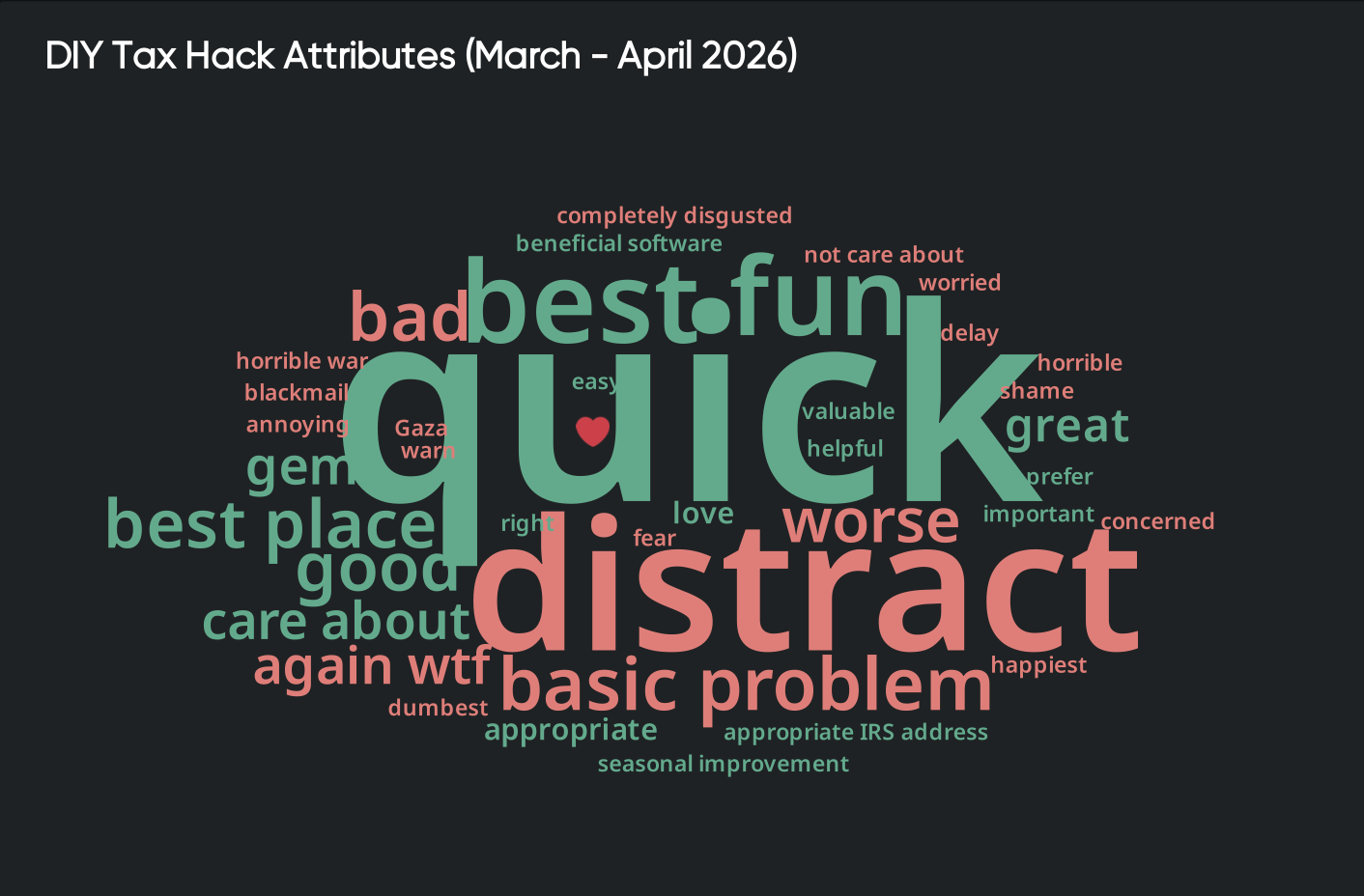

That standardization shows up clearly in the Quid dashboard data.

The dominant language around DIY tax tools includes terms like “easy,” “helpful,” and “valuable,” but it is not entirely frictionless. Words like “distract” and “problem” appear alongside them, signaling that the experience is manageable, not necessarily intuitive.

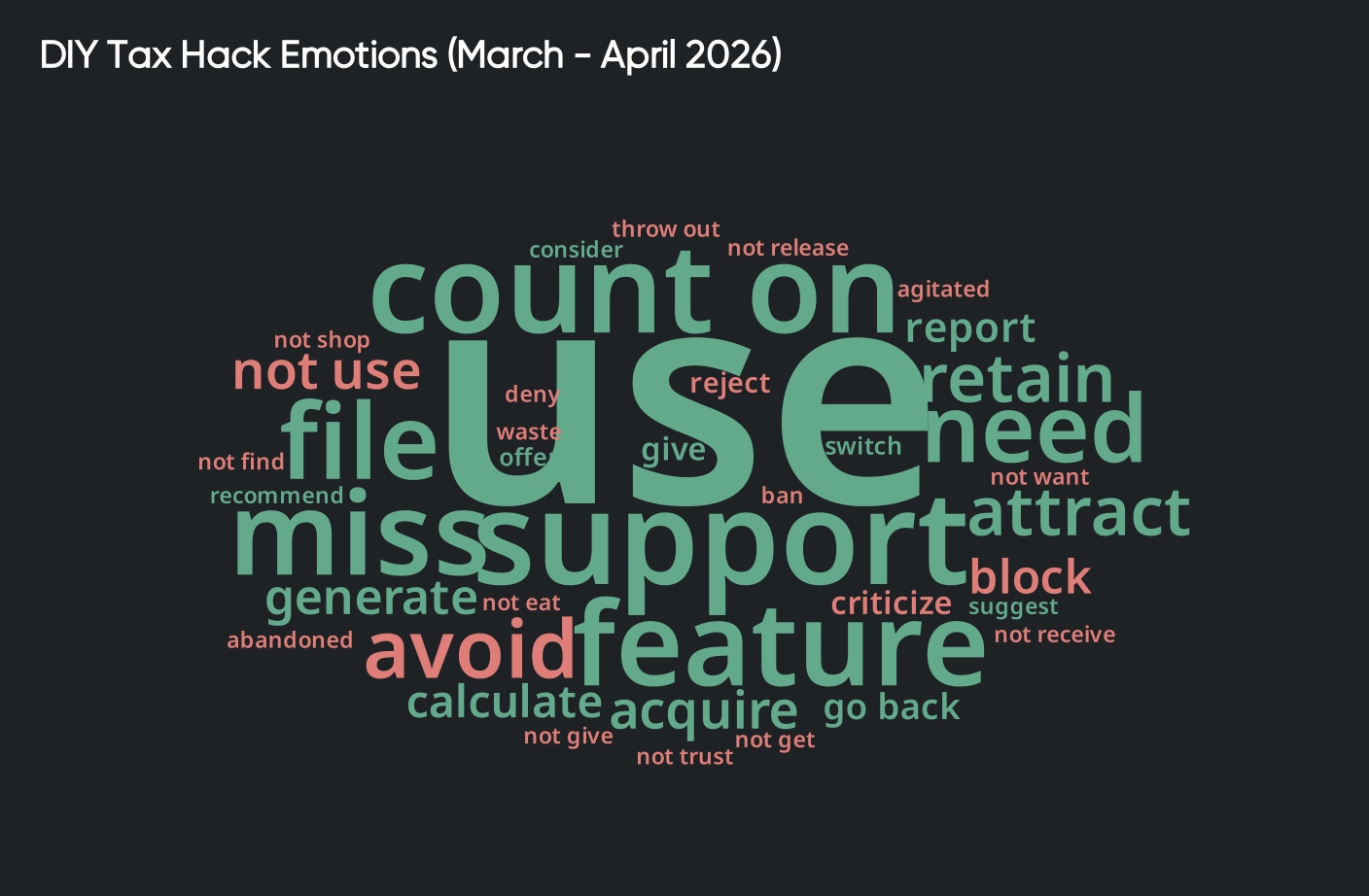

On the emotional side, the conversation clusters around “support,” “need,” “avoid,” and “calculate,” which points to a user base that is actively working through the process rather than confidently navigating it.

That distinction shows that people are not operating from deep understanding. They are operating within systems that guide them just far enough to complete the task.

Confidence is not driving this behavior; support is. And that holds across audiences.

This is not a single audience adopting DIY tax behavior. It is multiple groups moving in parallel, each driven by a different need.

From the Quid Agent cohort analysis, the behaviors split quickly once you look closer.

Each group is solving a different problem. They just happen to be using the same tools to do it.

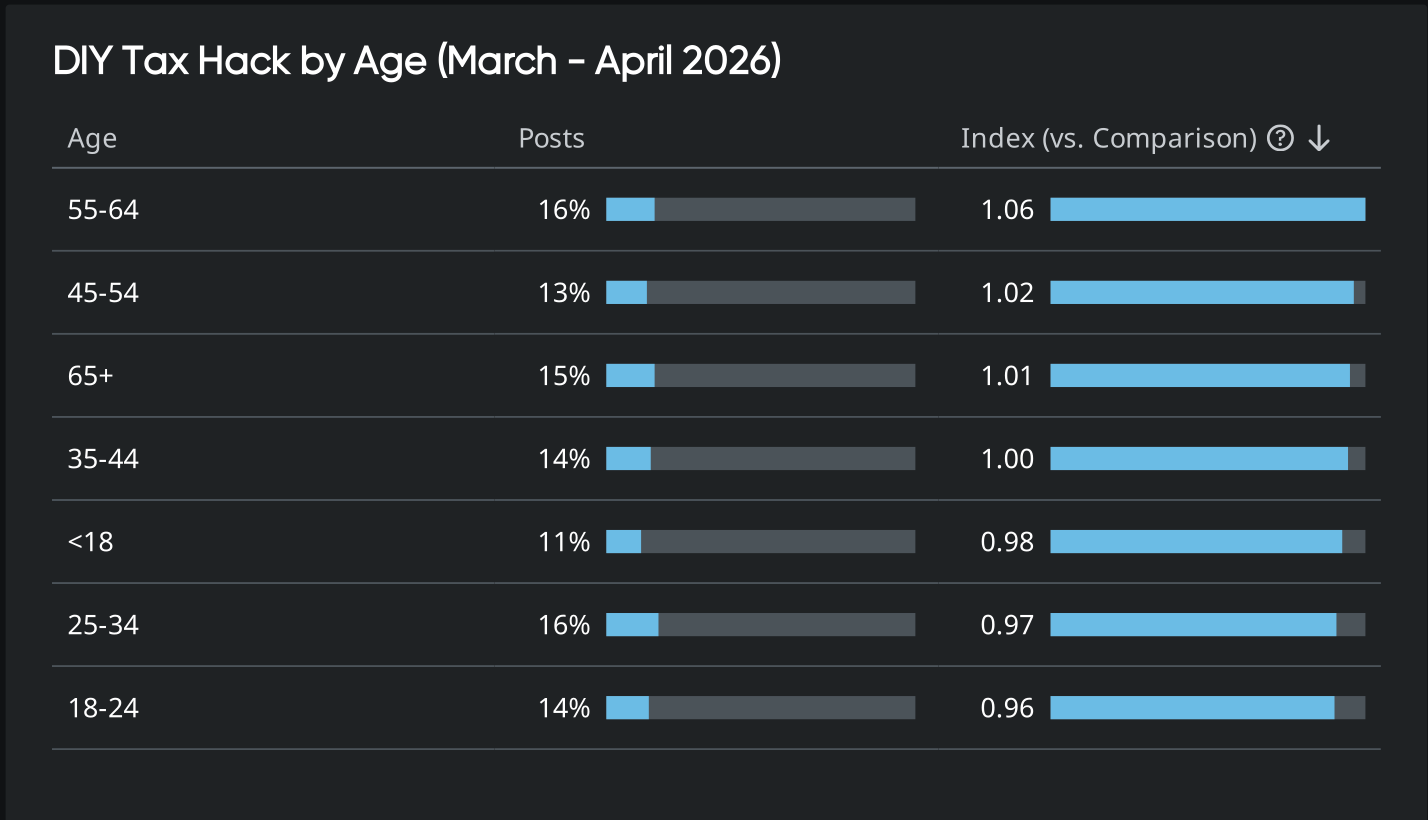

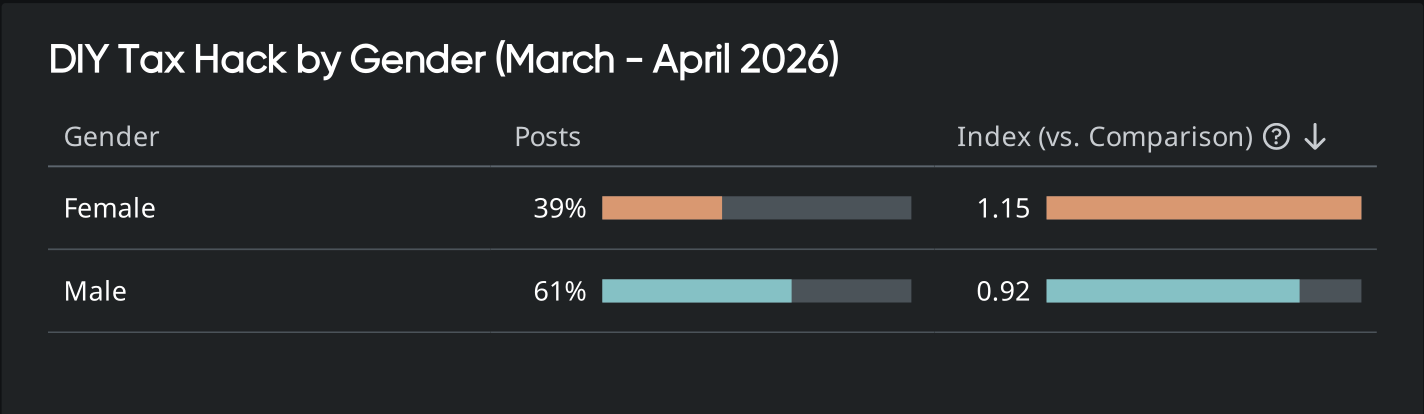

The Quid dashboard reinforces how broad this shift really is. Participation is distributed across age groups with no single segment dominating the conversation:

And while there is a slight male skew in volume, engagement is widespread.

That distribution is the signal.

DIY tax behavior is not being driven by a niche audience or a single use case. It is spreading across demographics, adapting to different financial situations, and scaling through shared tools and content.

And that is where the risk compounds. When multiple groups with different levels of complexity rely on the same simplified systems, errors do not remain isolated.

They scale with the behavior.

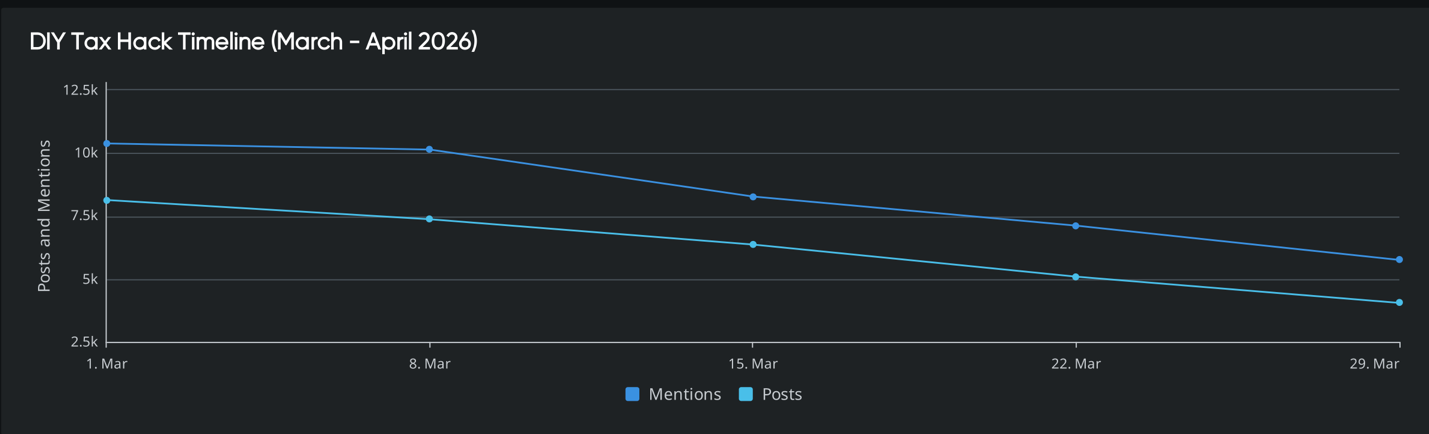

The behavior is not reacting to a single moment. It is repeating. From our dashboard timeline, mentions and posts trend steadily across March without sharp spikes or sudden drops. The pattern is gradual, controlled, and sustained rather than reactive.

That kind of consistency changes how this should be interpreted. This is not event-driven activity tied to deadlines, announcements, or viral moments. It reflects ongoing engagement. People are returning to the process, adjusting their approach, and continuing to participate over time.

The behavior is becoming routine as consumers refine, learn, and repeat.

The same ecosystem that enables DIY tax behavior also introduces risk at scale.

From the Quid Agent analysis, much of the viral “tax hack” content circulating across platforms contains partial truths. The core idea may be valid, but key eligibility requirements, thresholds, and constraints are often missing.

At the same time, scam activity is rising alongside adoption, and while IRS and FTC warnings are increasing, they move significantly slower than the content itself.

We see this tension reflected in the language being used. Alongside helpful and instructional terms, negative signals such as “fear,” “warn,” and other scam-adjacent language appear within the same conversation space.

This creates a clear tradeoff. The system offers faster access and lower friction, but it also increases exposure to error. The safeguards exist, but they are not keeping pace with the speed of distribution.

And despite that, behavior is not slowing. Consumers are choosing speed, even when accuracy is uncertain.

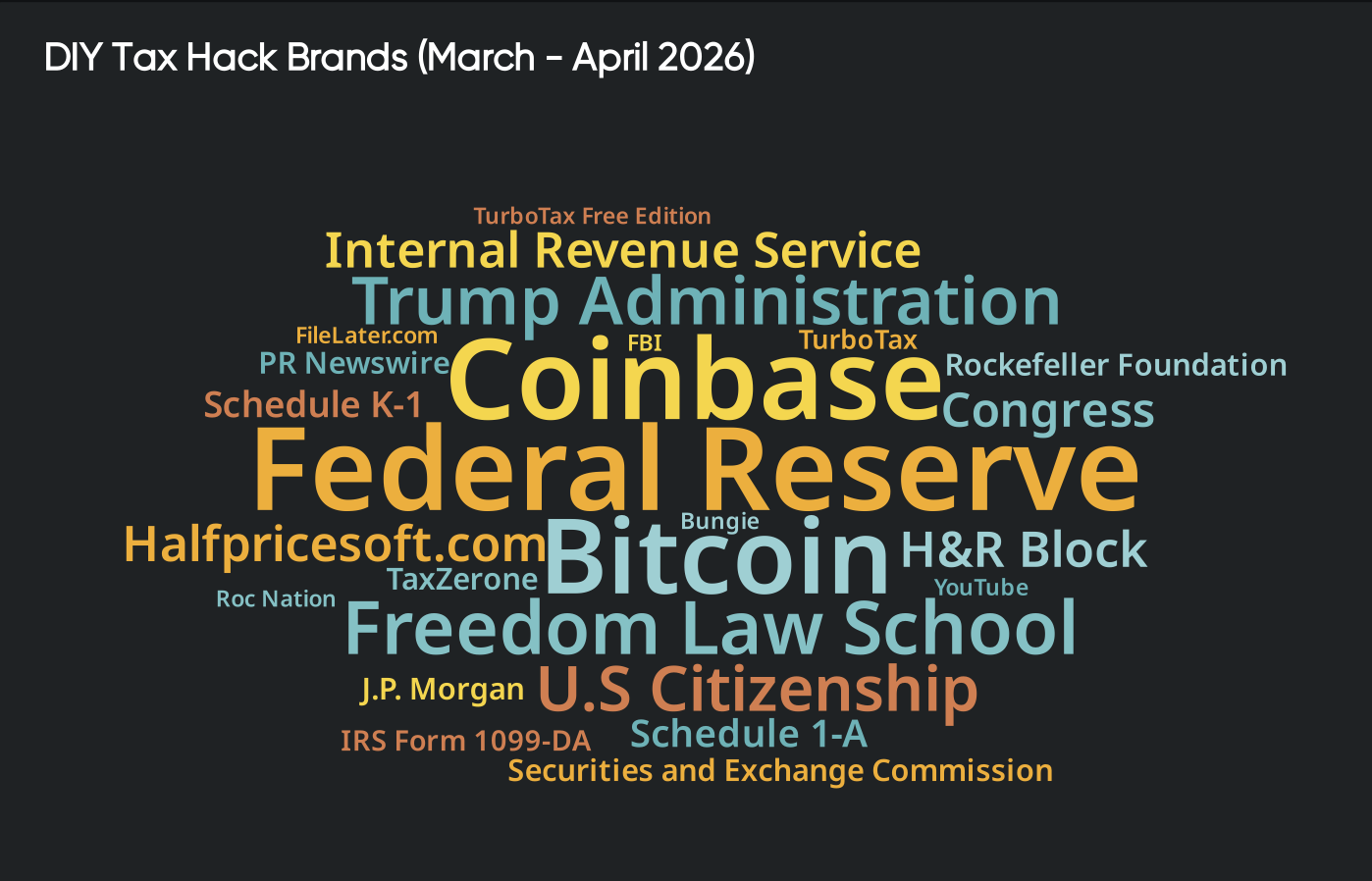

As DIY behavior scales, platforms are supporting and redefining the process. We uncovered brand associations showing tax software, financial institutions, and even adjacent financial entities appearing alongside content platforms within the same conversation.

That overlap signals a structural shift.

From the Quid Agent analysis, fintech platforms and tax tools are building ecosystems designed to capture and retain DIY behavior. APIs, automation layers, and integrated workflows are turning tax filing into a guided product experience rather than a standalone task.

Instead of asking a professional what to do, users are following prompts, recommendations, and automated checks built directly into the software. The guidance is coming from the product, not a person.

This is not a question of whether DIY tax behavior is good or bad. That decision has already been made at the consumer level. The behavior is established. It is scaling, and it is not slowing down.

What matters now is how it is shaping decisions.

Taken together, this creates a specific set of risks and opportunities.

Misinformation gains traction because it is easy to understand and quick to act on. Simpler explanations spread faster than accurate ones, especially when the rules are complex. At the same time, automation works well for straightforward cases but leaves gaps when filings require nuance. Those gaps are where errors happen.

Trust is also shifting. People are not defaulting to credentials or expertise. They are relying on whatever guidance is most immediate and easiest to follow. That might come from a platform, a creator, or a workflow built into the product itself.

This changes how decisions are made. Consumers are acting before organizations have full visibility into what influences them, so brands often respond after the behavior is already in motion.

Decisions are being shaped in real time, whether companies are tracking it or not.

Most teams will see the increased DIY adoption. They will see confusion or errors downstream, and changes in customer expectations. What they will not see clearly is how those behaviors formed, where they accelerated, or why certain narratives took hold over others.

That is the gap. Our team at Quid addresses that gap by connecting the signals that shape behavior before it becomes visible at the outcome level. We identify which narratives are gaining traction, where sentiment begins to shift from helpful to risky, how different cohorts interpret the same information, and when misinformation starts to outpace accurate guidance.

Reach out today to learn how we help brands understand how decisions are being influenced as they happen.